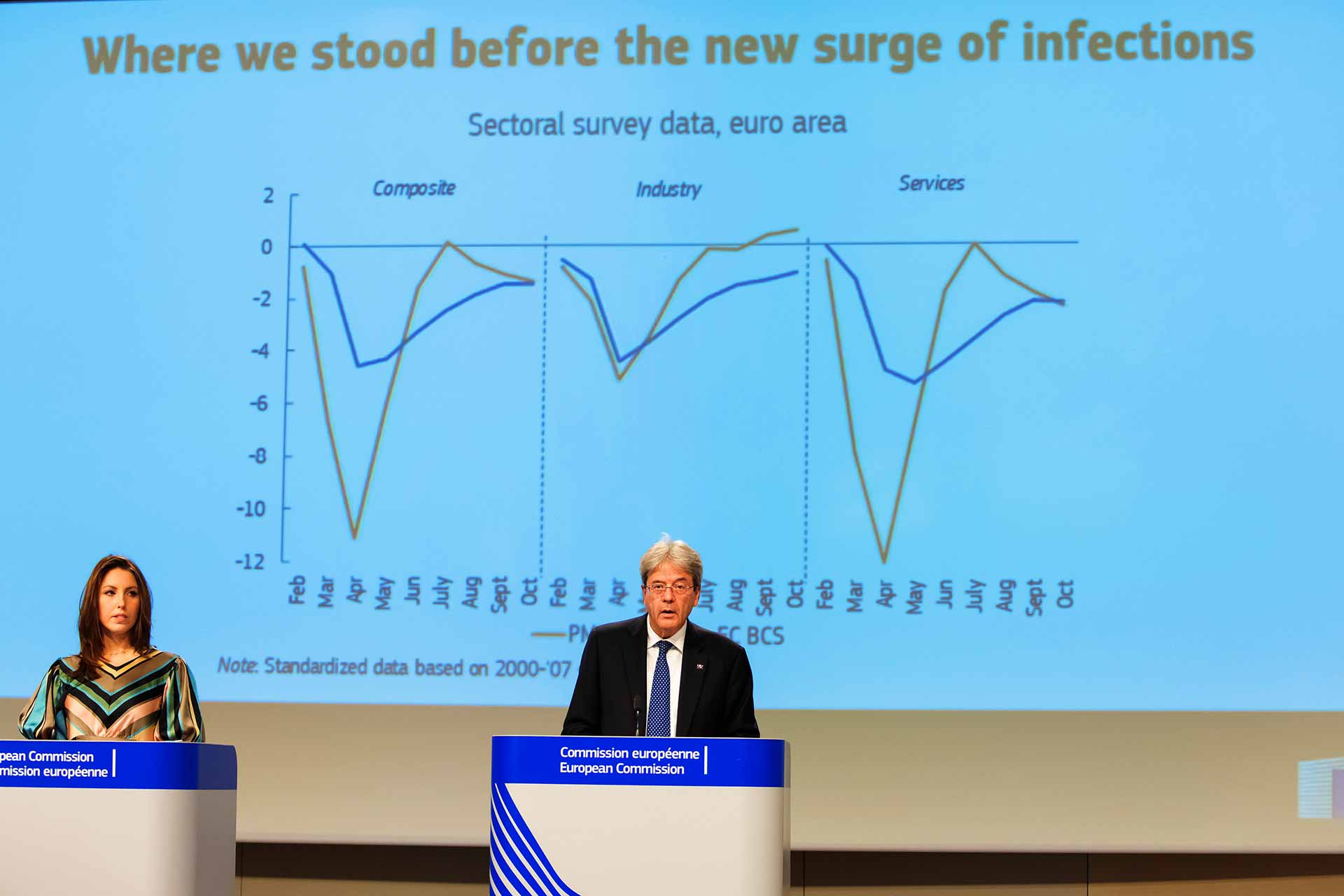

The coronavirus pandemic represents a very large shock for the global and EU economies, with very severe economic and social consequences. Economic activity in Europe suffered a severe shock in the first half of the year and rebounded strongly in the third quarter as containment measures were gradually lifted. Economic activity in Europe contracted sharply in the first half of the year.

COVID19 crisis with the important tourism sector bearing the brunt while domestic demand showed resilience. However, the resurgence of the pandemic in recent weeks is resulting in disruptions as national authorities introduce new public health measures to limit its spread. The epidemiological situation means that growth projections over the forecast horizon are subject to an extremely high degree of uncertainty and risks.

An interrupted and incomplete recovery

The Autumn 2020 Economic Forecast projects that the euro area economy will contract by 7.8% in 2020 before growing 4.2% in 2021 and 3% in 2022. The forecast projects that the EU economy will contract by 7.4% in 2020 before recovering with growth of 4.1% in 2021 and 3% in 2022. Compared to the Summer 2020 Economic Forecast, growth projections for both the euro area and the EU are slightly higher for 2020 and lower for 2021. Output in both the euro area and the EU wont probably recover its pre-pandemic level in 2022.

This forecast comes as a second wave of the pandemic is unleashing yet more uncertainty and dashing our hopes for a quick rebound.

Valdis Dombrovskis

The economic impact of the pandemic has differed widely across the EU and the same is true of recovery prospects. This reflects the spread of the virus, the stringency of public health measures taken to contain it, the sectoral composition of national economies and the strength of national policy responses.

Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People, said: “EU economic output will not return to pre-pandemic levels by 2022. But through this turbulence, we have shown resolve and solidarity. We have agreed unprecedented measures to help people and companies. EU will work together to chart the course to recovery, using every tool at our disposal. We agreed a landmark recovery package, NextGenerationEU – with the Recovery and Resilience Facility at its heart – to provide massive support to worst-hit regions and sectors. I now call again on the European Parliament and Council to wrap up negotiations quickly for money to start flowing in 2021 so that we can invest, reform and rebuild together.”

We agreed a landmark recovery package, NextGenerationEU – with the Recovery and Resilience Facility at its heart

Valdis Dombrovskis, Executive Vice-President for an Economy

The forecast was prepared in a context of severe uncertainty, with Member States announcing major new public health measures in the second half of October 2020 to limit the spread of the virus.

The forecast is based on the usual set of technical assumptions concerning exchange rates, interest rates and commodity prices, with a cut-off date of 22 October 2020. For all other incoming data, including information on government policies, this forecast takes into consideration information up until and including 22 October. Unless policies are credibly announced and specified in adequate detail, the projections assume no policy changes.

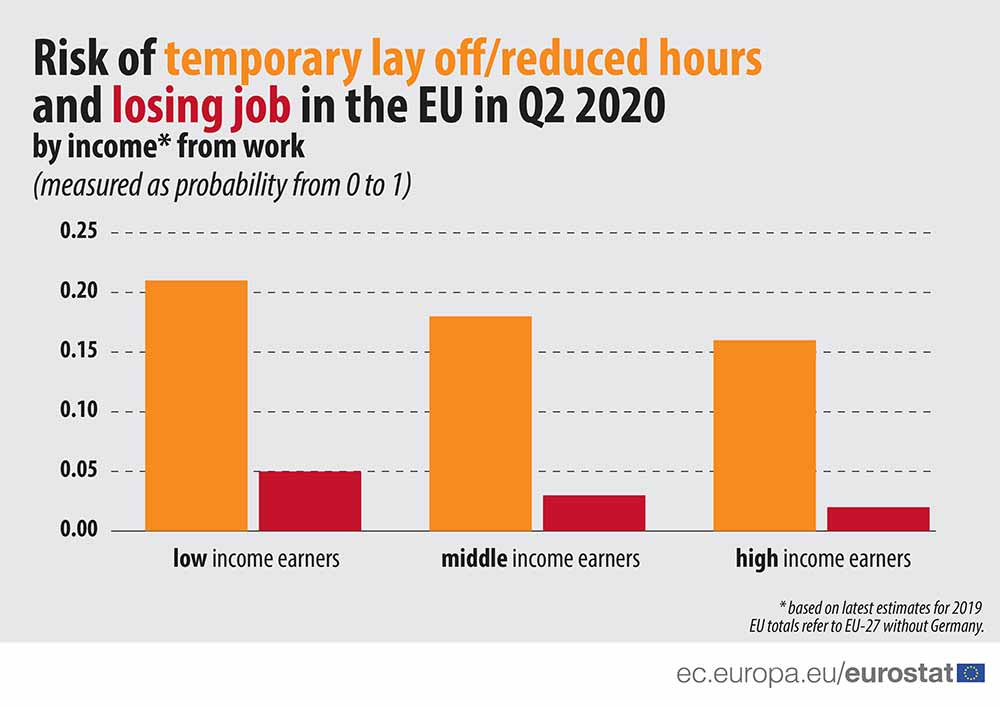

Rise in unemployment contained compared to drop in economic activity and European GDP

Job losses and the rise in unemployment have put severe strains on the livelihoods of many Europeans. Policy measures taken by Member States, together with initiatives at EU level have helped to cushion the impact of the pandemic on labour markets. The unprecedented scope of measures taken, particularly through short-time work schemes, have allowed the rise in the unemployment rate to remain muted compared to the drop in economic activity. Unemployment will continue rise in 2021 as Member States phase out emergency support measures and new people enter the labour market, but should improve in 2022 as the economy continues to recover.

COVID-19 research: The risk of losing your job and income in the EU

The forecast projects the unemployment rate in the euro area to rise from 7.5% in 2019 to 8.3% in 2020 and 9.4% in 2021, before declining to 8.9% in 2022. The unemployment rate in the EU will rise from 6.7% in 2019 to 7.7% in 2020 and 8.6% in 2021, before declining to 8.0% in 2022.

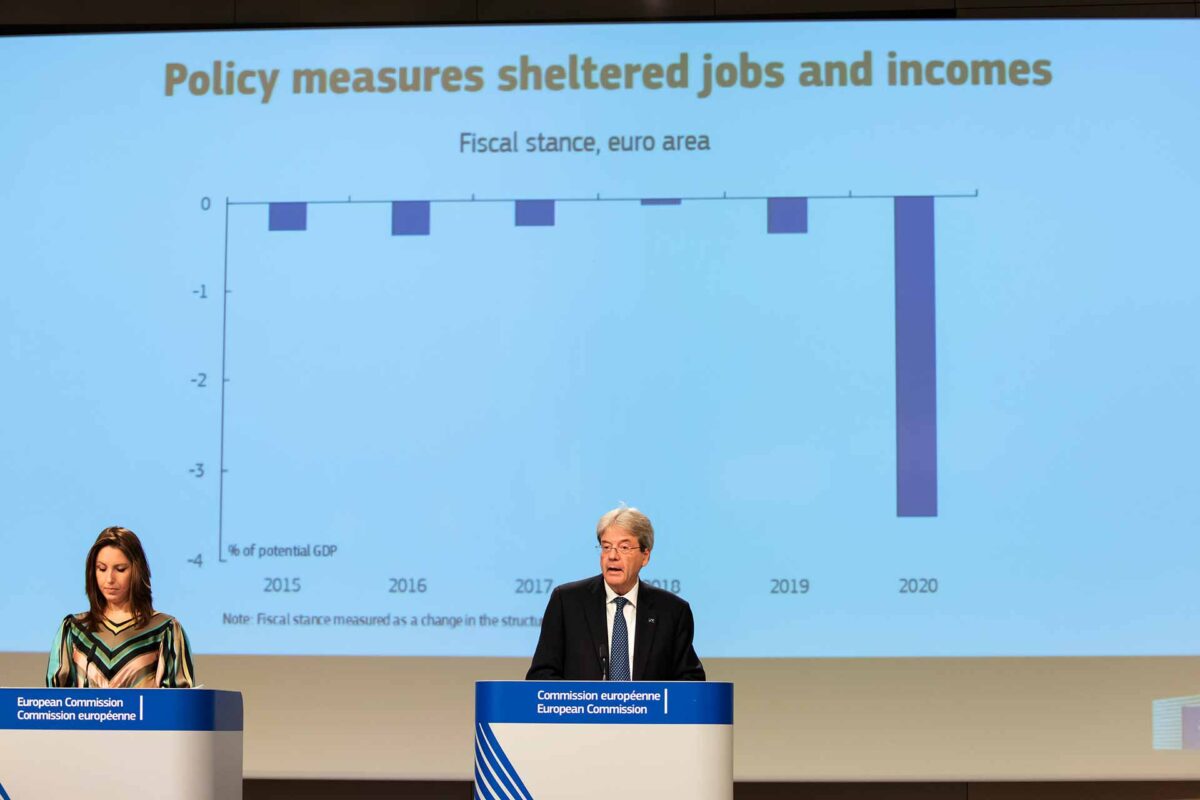

Deficits and public debt set to rise

The increase in government deficits will be very significant across the EU this year as social spending rises and tax revenues fall. Both come as a result of the exceptional policy actions designed to support the economy and the effect of automatic stabilisers.

The forecast projects the aggregate government deficit of the euro area to increase from 0.6% of GDP in 2019 to around 8.8% in 2020, before decreasing to 6.4% in 2021 and 4.7% in 2022. This reflects the expected phasing out of emergency support measures in the course of 2021 as the economic situation improves.

Mirroring the spike in deficits, the forecast projects the aggregate euro area debt-to-GDP ratio will increase from 85.9% of GDP in 2019 to 101.7% in 2020, 102.3% in 2021 and 102.6% in 2022.

Growth will return in 2021 but it will be two years until the European economy comes close to regaining its pre-pandemic level.

Paolo Gentiloni

Paolo Gentiloni, Commissioner for Economy, said: “After the deepest recession in EU history in the first half of this year and a very strong upswing in the summer, Europe’s rebound has been interrupted due to the resurgence in COVID-19 cases. Growth will return in 2021 but it will be two years until the European economy comes close to regaining its pre-pandemic level. In the current context of very high uncertainty, national economic and fiscal policies must remain supportive, while NextGenerationEU must be finalised this year and effectively rolled out in the first half of 2021.”

Inflation remains subdued

A steep fall in energy prices pushed headline inflation into negative territory in August and September. Core inflation, which includes all items except energy and unprocessed food, also fell substantially over the summer due to lower demand for services, especially tourism-related services and industrial goods. Weak demand, labour market slack and a strong euro exchange rate will exert downward pressure on prices.

Inflation in the euro area, as measured by the Harmonised Index of Consumer Prices (HICP), is forecast to average 0.3% in 2020, before rising to 1.1% in 2021 and 1.3% in 2022, as oil prices stabilise. For the EU, inflation is forecast at 0.7% in 2020, 1.3% in 2021 and 1.5% in 2022.

A high degree of uncertainty with downside risks to the European GDP outlook

Uncertainties and risks surrounding the Autumn 2020 Economic Forecast remain exceptionally large. The principal risk stems from a worsening of the pandemic, requiring more stringent public health measures and leading to a more severe and longer lasting impact on the economy. This has motivated a scenario analysis for two alternative paths of the pandemic evolution – a more benign one and a downside one – and its economic impact.

Rebound interrupted as resurgence of pandemic deepens uncertainty

There is also a risk that the scars left by the pandemic on the economy – such as bankruptcies, long-term unemployment and supply disruptions – could be deeper and farther reaching. The European economy could also be impacted negatively if the global economy and world trade improved less than forecast or if trade tensions were to increase. The possibility of financial market stress is another downside risk.

On the upside, NextGenerationEU, the EU’s economic recovery programme, including the Recovery and Resilience Facility, is likely to provide a stronger boost to the EU economy than projected. This is because the forecast could only partially incorporate the likely benefits of these initiatives, as the information available at this stage on national plans is still limited.

BREXIT Deal or NO-Deal

A trade agreement between the EU and the UK would also have a positive impact on the EU economy from 2021 compared to the forecast baseline of the UK and EU trading based on WTO Most Favoured Nation (MFN) rules.

EU cuts 2021 economic outlook as virus spreads

As COVID-19 cases keep rising, the European Union’s executive commission lowered its forecast for the economic rebound from the coronavirus pandemic next year and said the economy wouldn’t reach pre-virus levels until 2023. According to the forecast, in the first half of the year, economic activity declined sizeably by 5.5% y-o-y, dragged by the impact of the COVID-19 crisis and accompanying lockdown measures.

The European Commission’s next forecast will be an update of GDP and inflation projections in the Winter 2021 Economic Forecast, which is expected to be presented in February 2021.

{kind=link}